One of the biggest advantages that individual investors have is their ability to maintain a long-term time horizon. Professional investors can take advantage of this edge as well, but few do. I’ve long believed that the modern day advantage in markets is not informational advantage or even analytical skills, but rather behavioral. Being a great business analyst is table stakes of course, but that’s a necessary, not sufficient condition for success in investing. What separates the great investors from the average is all about behavior.

Being patient and thinking long-term is widely discussed as a positive attribute. It’s not debatable. I’ve never heard an investor say they are impatient and short-term focused. But the fact that this is widely talked about does not mean it is widely practiced. Much like the principle of “hard work”, it’s easier said than done. The vast majority of people in business would say they are a hard worker, but the reality is only 10% of those people are in the top 10% on the spectrum of work ethic. The same goes for behavioral advantages in investing. The vast majority of people say they have this edge, but the facts suggest that few actually implement it.

I recently read through the letters of Nick Sleep, who ran a very successful investment fund in the United Kingdom before closing it last decade. Sleep is a great thinker and I highly recommend his work. One thing Sleep wrote a lot about is how the average holding time period for many of the stocks he owned was around 50 days, whereas he planned to hold these stocks for more than 250 weeks (5 years). I think his key observation is important: The marginal buyer who is holding a stock for 2 months is not placing much emphasis on that company’s competitive advantage because that advantage won’t matter much at all over the next few months; what matters over that period of time are things like market perception, news flow, sentiment, and perhaps short-term business momentum.

Truly Understanding the Source of Enduring Business Success

So what Sleep did is he decided to compete in a different game. Instead of attempting to determine how the crowd will react this quarter or how the trajectory of the business will fare this year, he wanted to focus on the factors that contributed to a business’s ultimate potential. What attributes give this company an advantage? What will lead this company to success through both good times and bad times (because if you’re a long-term shareholder, all companies face headwinds at some point).

Walmart’s Cost Advantage — An Enduring Advantage

Sleep used the example of Walmart’s cost advantage. Walmart’s business model was to offer the lowest prices on everyday merchandise, and steadily gain scale advantages through larger and larger bulk purchases from suppliers at lower and lower unit prices, which meant further savings to customers, which led to more growth and more scale advantages. Sleep coined a term for this business model: “scaled economies shared”, meaning the business gained scale, but instead of keeping the excess profits for itself, it gave these scale advantages to the customer in the form of lower prices. This sacrificed near term profits but led to far greater future profits, which of course is where value comes from.

Walmart, Costco, and Amazon all exhibit this basic business model, and all have achieved great success. But what Sleep noticed is that investors — even when they understood this business model — still undervalued all of these companies because they placed too much emphasis on shorter term factors such as seasonal same-store sales trends, quarterly margins, or the business cycle. All of this focus came at the expense of what really mattered, which was the cost advantage that was so hard for competitors to replicate.

NVR’s Enduring Advantage

I started on a project of going through my own watchlist to spend time thinking about each “source of enduring business success” for the companies I follow.

NVR is a homebuilder that restructured its business in 1993 after facing one of the inevitable downturns in an industry defined by booms and busts. I believe NVR has three distinct “sources of enduring business success”:

- Land light business model — unlike most builders, NVR doesn’t develop or hold its own land on its balance sheet. Instead, it partners with 3rd party land developers who take a portion of the gross profits in exchange for removing NVR’s risk of holding too much land during a downturn. NVR essentially pays developers to take on the capital intensity (and the debt and the risk) that is naturally part of the home building business. The result is much faster inventory turns, 40% returns on capital, and excess free cash flow in good times and bad.

- Efficient operations — like the great retailers mentioned above, NVR’s cost efficiencies are a very under appreciated advantage in their business. They operate factories near the communities which act like distribution centers. This drives efficiencies and economies of scale. NVR’s operating costs are just 5% of sales — about half the costs of their peers.

- Incentives and Culture — most of the NVR executive pay comes from options that are granted based on economic profit and returns on capital, not simply growth. Most other builder execs get bonuses based on EBITDA or revenue growth. This makes it very hard for these builders to give up the profits (and the risk) that come from land development because it means willingly accepting less profit (even if that means much higher returns on capital, more free cash flow, and ultimately better value creation). As Buffett says, the best way to make a savings account grow is add more money to it, but this doesn’t increase the rate of return the account holder receives. Builders can easily juice revenue and profit by taking on more debt to buy land, but this doesn’t always (in fact rarely) leads to great value creation or stock price performance in the long run. (Last note on culture: NVR has never “repriced” its options lower, which is the habit of many companies who pay their employees in stock.)

The result of these attributes have led to one of the great stocks of the last 30 years. NVR has gone from $9 when they restructured in 1993 to over $4,700 today, and it has repurchased 78% of its shares over that stretch.

It is my opinion that the three of these advantages working together have created a business model at NVR that is very hard to copy. It’s not just the land light model on its own; it’s the culture of efficiency, the focus on ROIC, and the long-term thinking. NVR’s CEO just announced his retirement after 40 years at the helm (he’ll move to Chairman). The proxy statement reads like a family history. Multiple executives have been with the company for decades, and this longevity can sometimes create a special “way of doing business” that can’t simply be cloned overnight.

In short, NVR has multiple sources of enduring business success. Will they sell fewer homes this year if the supply chain remains constricted? Most likely. Are they subject to the same economic or interest rate pressures that other builders are? Yes. But will they be a company still earning world-class returns on capital a decade from now? I think the latter question matters more to long-term investors, and the answer to that question has to be found through analyzing the strength of those more permanent attributes that don’t change with the cyclical economic tides.

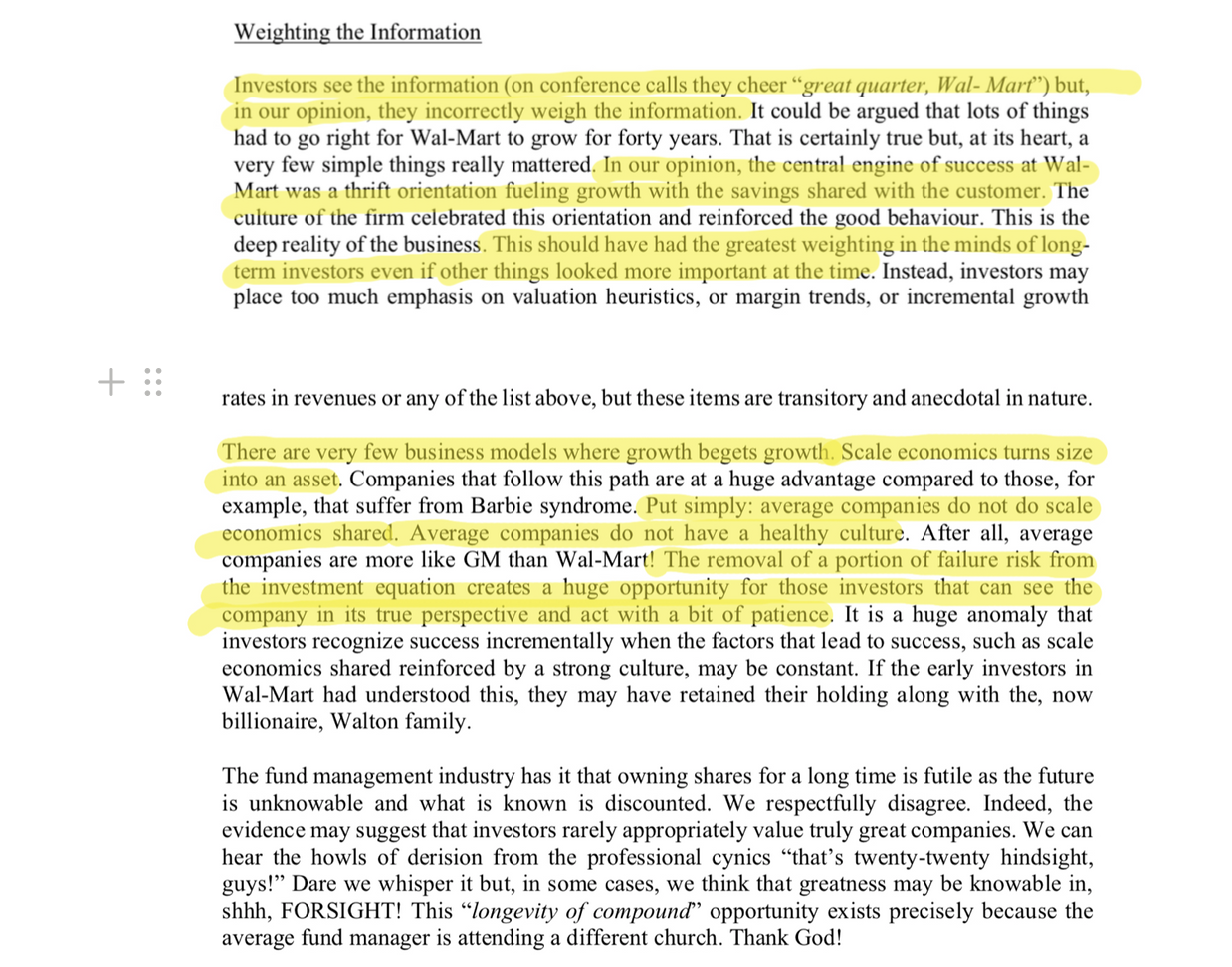

“Weighting the Information”

Last summer, investors sold Amazon after its Q2 earnings report because the next few quarters would face tough comps from the gangbuster 2020; but Amazon’s value in 2032 has little to do with the comps it faces in 2022. It has a lot to do with the durability of its network, the economies of scale, the distribution advantages, the culture of operational excellence; none of that will likely drive the stock this quarter, but it’s what matters most to the stock over the next decade.

A mismatch of time horizons lead some investors to more heavily weight the short-term and deemphasize these sources of “enduring business success”.

Investors who hope to buy a stock that will rise this year are much less apt to fully value these types of sustainable long-term competitive advantages. And fortunately for investors with 5-10 year time horizons, this creates a lot of opportunity. I’ve always felt that durable growth (not necessarily fast growth, but long-lasting durable growth) often gets undervalued by the market. I think Nick’s point about time horizon goes a long way to explaining why.

Summary – Focus on the Advantages that will Matter in a Decade

The key variable for these companies was not what the comparable sales will look like next quarter or what the business might earn next year. The key variable was the durability of the cost advantage. This advantage didn’t change much from year to year. In fact it likely increased over time, which is a unique business model where growth actually perpetuates more growth.

I wanted to share a clip from my notes on this section of Nick’s letters:

This post got me thinking about making a list of companies that have sources of enduring business success. I’m currently going through Saber’s database of companies I’ve studied to build a list of what I believe are the top 50 companies in the world, along with a contenders list of companies I think will be the next generation’s top 50. A key part of this exercise is spending a lot of time thinking about these “sources of enduring business success”.

John Huber is the founder of Saber Capital Management, LLC. Saber is the general partner and manager of an investment fund modeled after the original Buffett partnerships. Saber’s strategy is to make very carefully selected investments in undervalued stocks of great businesses.

John can be reached at john@sabercapitalmgt.com.