A couple weeks back I wrote a quick post on Tom Gayner, who is an outstanding investor and head of Markel (MKL), one of my favorite companies in America. Markel is a well run insurance company that has been compounding shareholder equity consistently at about 16% per year over the past 20 years. MKL operates with a similar business model to that of Berkshire Hathaway:

- Write insurance policies to collect premiums

- Invest the float

Insurance companies make money in those two main categories: underwriting profits and investment profits. Many insurance companies actually lose money writing insurance, but make money on investments. It’s very difficult for insurance companies to produce consistent underwriting profits. The best insurance companies are profitable over time in both their underwriting and their investments.

MKL has been achieved an underwriting profit in 14 of the last 20 years, and has an average combined ratio well under 100% (under 100% is profit) over the past 2 decades. The beautiful thing about running a profitable insurance business is that the float is free and permanent (float is an insurance term which very generally means the temporary funds that the company controls after accepting premium payments but before paying out claims). As long as the underwriting is profitable, this float will act as an interest free loan that never has to be paid back, thus allowing it to be invested in long term securities such as stocks and bonds.

This is where we become even more interested in MKL. Tom Gayner is an outstanding investor. I recommend reading his shareholder letters, which contain a wealth of knowledge on both the investment front as well as the insurance business.

Gayner is a classic Buffett investor: he loves buying great businesses at fair prices. Here at BHI, we love cheap stocks, and we’re looking for significant absolute returns over time… we are trying to study Buffett from the 50’s and 60’s more than Buffett of the 80’s and 90’s, but every value investor loves great businesses and it’s worth studying the way investors like Gayner think.

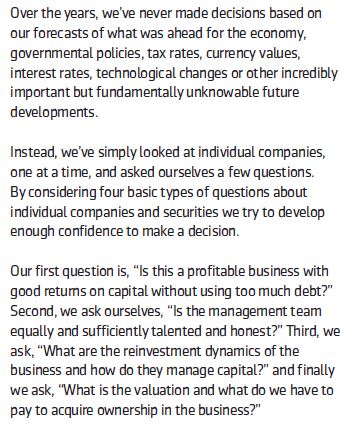

And the way he thinks? Very simply. No macro economic forecasting, no complex spreadsheets, just simple logic and sound principles. Here is Gayner describing his own investment philosophy:

This simple process has allowed Gayner to beat the S&P 500 over time by taking much less risk of permanent capital loss. This investment method combined with a profitable underwriting discipline has led MKL to compound book value at 16% per year. Currently MKL is priced at a 30% premium to book value, and I think it’s probably worth that. MKL is on my great company watchlist, and if it falls to book value or below, it’s likely to be an outstanding long term investment that will allow shareholder returns to match or exceed book value growth over time.

This simple process has allowed Gayner to beat the S&P 500 over time by taking much less risk of permanent capital loss. This investment method combined with a profitable underwriting discipline has led MKL to compound book value at 16% per year. Currently MKL is priced at a 30% premium to book value, and I think it’s probably worth that. MKL is on my great company watchlist, and if it falls to book value or below, it’s likely to be an outstanding long term investment that will allow shareholder returns to match or exceed book value growth over time.